Industry leaders are turning away from the traditional group insurance model and instead offering employees ICHRA, which allows for more customizable health insurance.

Michele Grant, the CEO of Block and Tackle, felt fed up with the insurance options she was forced to offer her employees in 2022.

Every year, insurance costs rose for the small marketing strategy firm, and the back-end work for Grant did not outweigh the benefits for her employees.

Michele Grant

CEO, Block and Tackle

“I remember Googling, ‘How can we offer personalized health benefits?’” Grant said. “There’s got to be a better way to do this.”

She quickly found her answer with an Individual Coverage Health Reimbursement Arrangement, or ICHRA, in which employers provide employees with a fixed monthly allowance to buy their own health insurance. Those employees then go to the individual market and purchase health plans that work for them.

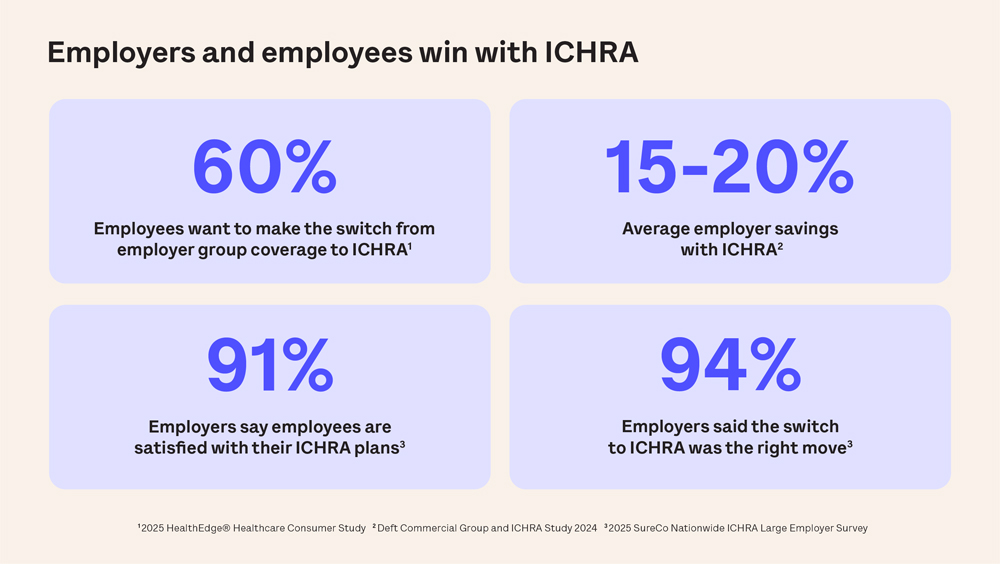

This model, launched in 2020, is gaining popularity. More than 260,000 employees in the United States use this model, and the trend has grown 1,000% in the past six years, according to the HRA Council.

Employers like Grant are opting for this unique approach to insurance. Now, both employers and employees say it’s the insurance of the future.

The traditional insurance model is dated

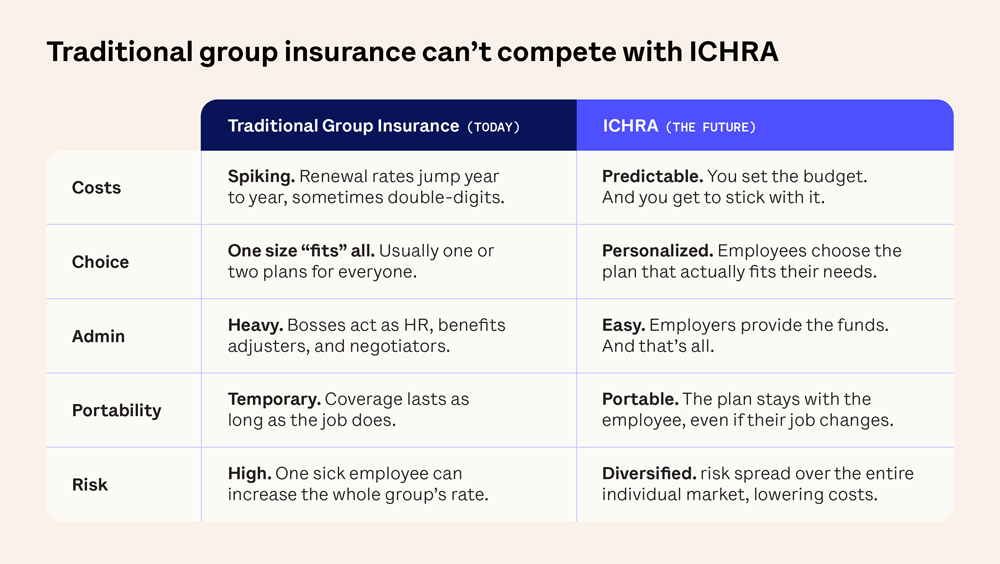

The employer-sponsored health insurance approach is the norm for most companies in the United States. In this model, employers typically offer two or three plans for employees to choose from during open enrollment.

There’s one big problem here: The options given to employees are broad and not tailored to individual health needs, even though employees have different health situations.

Louis DeStefano, the Chief Growth Officer at Oscar Health, an insurance company leading the movement toward ICHRA, says employers face the daunting task of choosing a small number of plans — often as many as three — to try to fit the needs of every one of their employees.

Louis DeStefano

Chief Growth Officer, Oscar Health

“The employer group model is one-size-fits-all. It could be very traumatic for the one or two families who need specific medications or providers,” DeStefano said. “Consumers don’t have a choice on how to spend their dollars.”

But there are other issues with this employer group model as well. For starters, companies are always subject to ever-increasing costs. Healthcare costs in the United States are growing faster than the rate of inflation and wage growth. Both employers and employees are living with high single- and double-digit increases every year. Grant said she vividly remembers the “horror I felt” when her company’s insurance costs went up 42%.

That’s normal in the group model. In fact, the average family premium for employer-sponsored health insurance topped $26,000 in 2025, according to KFF’s latest health benefits survey. In many cases, families are now spending more on their healthcare than on their mortgages.

Grant had other issues with the group insurance model, especially the rigidity.

“It’s very difficult to shop for group plans as an employer,” she said, “because you don’t know everybody’s doctors, and you don’t know everybody’s prescription profiles.”

Often, employees have to change doctors each year to find one in-network with the group plan.

On the individual market, between 2018 and 2024, premium prices went up near zero percent. Meanwhile, the premiums on employer plans climbed 4.26%.

Although Grant’s company, Block and Tackle, is located in Atlanta, a lot of her employees are based all over the country, especially after the pandemic. This only further complicated matters for her.

ICHRA has solved all these issues — for both employees and employers.

Employees get to choose the health plan that is right for them

The greatest advantage of ICHRA is that employees can purchase plans that fit their needs on the individual marketplace.

Here’s how it works: Employers provide employees with a fixed monthly allowance to buy their own health insurance. This is comparable to the amount the employer subsidized in the traditional group model. The employee then uses that money to purchase plans that meet their health needs. Employees have access to benefit tools that help them choose from hundreds of plans to find what is right for them. There are even plans built around treating specific conditions such as diabetes or COPD.

“Say an employer wants to spend $75 on a Christmas gift. The employee picks what $75 gift they get,” Grant said. “It’s exactly the same.”

DeStefano noted that workers might be looking for plans that cover treatments for specific health concerns, such as diabetes, infertility, or mental health. For example, Oscar offers Hello Meno, which allows women to purchase plans tailored to their needs during menopause. It also offers plans specifically for chronic conditions.

“If you want to buy a virtual physical therapy option, you can,” DeStefano said. “Those are some of the customizable, curated products around healthcare that you can buy under the ICHRA model. … It gives more power to the employees.”

Employers can customize ICHRA to their specific needs

Grant said she understands that some CEOs or small business owners might be curious about switching to ICHRA, but they might fear the unfamiliar and nontraditional insurance strategy. She said that shouldn’t be the case. Switching to ICHRA simplifies the benefit cycle for employers who can use one platform to handle all plan vetting, enrollment, onboarding, and payments for employees. It also takes employers out of a process they don’t want to control for their employees.

ICHRA also allows for a level of personalization not found in group insurance. Employers can customize eligibility by employee group (e.g., full-time, part-time, seasonal) and can even have 50 employees with 50 different plans across multiple states with no additional administrative headache.

“ICHRA is grounded in the marketplace and gives you the flexibility to treat everyone equally,” Grant said. “If you read up on it, you’ll realize how it’s a sensible, even more straightforward choice.”

Grant did point out, however, that while the process is easier for the employer, she had to provide internal education to help her workers understand what this new insurance model entails. But once everyone understood, all her employees were on board.

“I don’t get any complaints about our health benefits anymore,” Grant said. “I haven’t heard a complaint in two years.”

It is clear that employees are happier, healthier, and more productive because they are buying what is best for them. In fact, a study shows ~91% of companies report strong employee satisfaction moving to the individual market model, and ~95% of employers say switching to the individual market was the right decision.

While larger employers often do strive to offer multiple plan options and point solutions to meet the diverse health needs of their employee populations, they’re constantly playing Whack-a-Mole trying to support another new population where health costs are rising or more employees are being diagnosed.

By giving employees choice about their health plans, employees can choose richer plans that will help ensure they get coverage for their higher cost conditions.

Employers can get started with Oscar

If you’re an employer, like Grant, who wants to empower your employees and offer them options that better support them, you can start with Oscar.

All you have to do is head to Oscar’s website and answer a few questions, including the state your company is located in and the number of full-time employees you have. Oscar will handle the rest, and you’ll get quotes in under five minutes.

“As an employer, you have a responsibility to take care of your employees,” Grant said. “It starts with us as employers doing right by our employees.”

Head to hioscar.com/ichra to find out how you can get started with ICHRA at your company today

Oscar Medical coverage is underwritten by Oscar Insurance Company and its affiliates. Administrative Services for all plans provided by Oscar Management Corporation. All insurance policies and group benefit plans contain exclusions and limitations. For availability, costs, and complete details of coverage, contact Oscar at 855-672-2788.